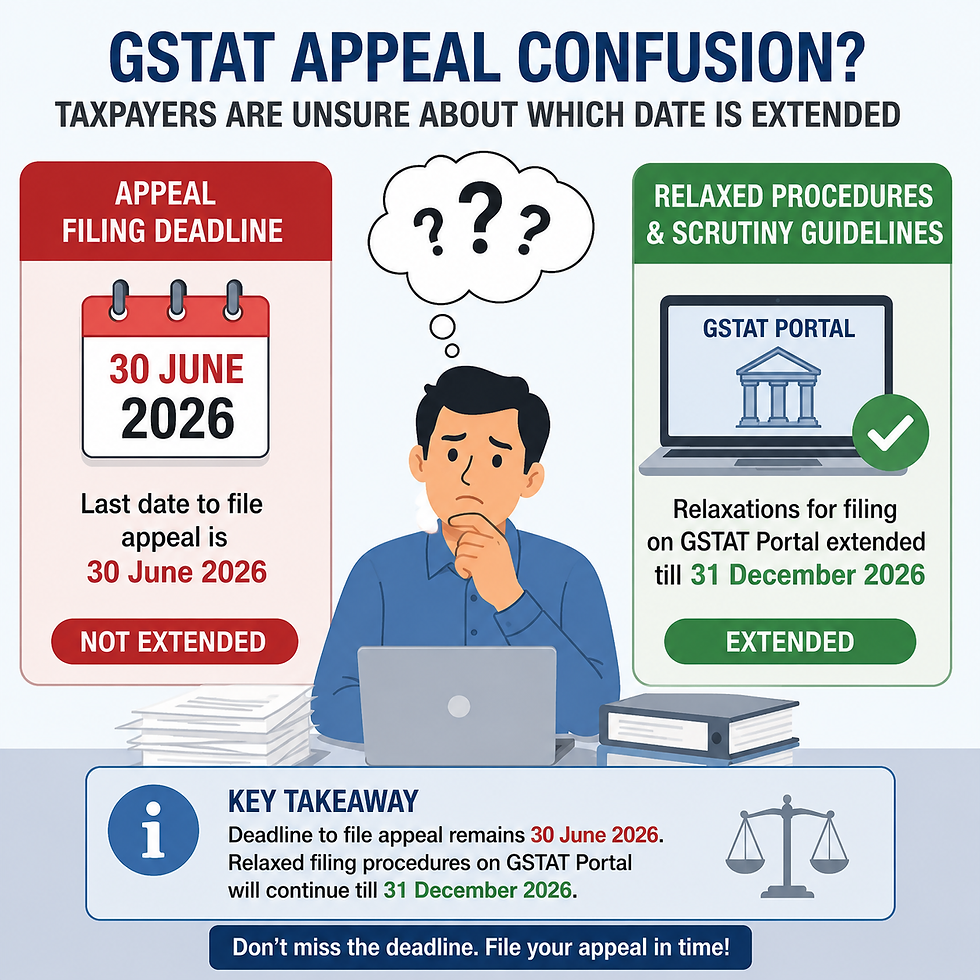

GSTAT extends procedural relaxation norms till 31st December 2026. (Note : Appeal filing date not extended)

- AMEY SHARMA

- May 14

- 2 min read

Order F.No. GSTAT/Pr.Bench/Portal/125/25-26 dated 14 May 2026

The Goods and Services Tax Appellate Tribunal (GSTAT) has taken a taxpayer-friendly step by extending the procedural relaxations relating to appeal filing through the GSTAT Portal till 31 December 2026. This extension is intended to mitigate the practical difficulties being experienced by taxpayers, advocates, chartered accountants, and departmental officers during the initial phase of implementation of the Tribunal's online filing system.

Background

The GST Appellate Tribunal has recently commenced operations and introduced a digital platform for filing appeals. Recognizing the transitional challenges faced by stakeholders, GSTAT had earlier issued Order No. 16/2026 dated 20 January 2026 and subsequent instructions dated 10 March 2026 providing certain procedural relaxations.

Considering that many taxpayers continue to face technical and procedural difficulties while filing appeals electronically, the President of GSTAT has exercised powers under Rule 123 of the GST Appellate Tribunal (Procedure) Rules, 2025 and directed that these relaxations shall continue till 31 December 2026.

Important Directions for Scrutiny Officers

The order specifically instructs Registrars, Joint Registrars, Deputy Registrars and Assistant Registrars responsible for scrutiny of appeals to adopt a practical and facilitative approach.

Where Form APL-05 contains soft copies of the following documents, scrutiny officers should not raise defects merely on procedural grounds:

Show Cause Notice (SCN)

Order-in-Original (OIO)

Order-in-Appeal (OIA)

Statement of Facts

Grounds of Appeal

Proof of Pre-deposit

Court Fee payment details wherever applicable

Importantly, no Court Fee or Pre-deposit is required in appeals filed by the Revenue Department.

Digital Verification Requirement

The order further clarifies that one verification and digital signature of the appellant is required while filing the appeal through the GSTAT Portal.

This reinforces the Tribunal's emphasis on digital authentication while keeping procedural requirements simple and practical.

Practical Impact for Taxpayers and Professionals

The extension of these relaxations is a major relief for taxpayers and tax practitioners. In the initial phase of any new digital system, procedural hurdles often lead to rejection or delay in registration of appeals. The present instructions seek to minimize such technical objections and ensure that genuine appeals are not dismissed on avoidable procedural grounds.

For Chartered Accountants, Cost Accountants, Advocates and GST Consultants handling appellate matters, the order provides greater certainty regarding acceptable documentation and reduces the risk of defect memos being issued for minor procedural issues.

Conclusion

The GSTAT's decision to extend the relaxed filing framework till 31 December 2026 reflects a pragmatic and taxpayer-centric approach. By permitting soft copies, accepting scanned certified orders, and restricting unnecessary defect objections, the Tribunal has demonstrated its commitment to ensuring smooth access to appellate remedies during the transition to a fully digital dispute resolution system.

Taxpayers and professionals should nevertheless ensure that all substantive documents, authorizations, digital signatures, and statutory requirements are properly complied with while filing appeals so that matters can proceed without avoidable delays.

NOTE :

The procedural relaxations have been extended till 31 December 2026, but taxpayers should continue to treat 30 June 2026 as the last date for filing eligible GSTAT appeals unless a separate notification extends that deadline.

Comments